Excessive rates of interest haven’t crashed the monetary system, set off a wave of bankruptcies or triggered the recession that many economists feared.

However for hundreds of thousands of low- and moderate-income households, excessive charges are taking a toll.

Extra Individuals are falling behind on funds on bank card and auto loans, whilst many are taking over extra debt than ever earlier than. Month-to-month curiosity bills have soared because the Federal Reserve started elevating rates of interest two years in the past. For households already strained by excessive costs, dwindling financial savings and slowing wage development, elevated borrowing prices are pushing them nearer to the monetary edge.

“It’s loopy,” stated Ora Dorsey, a 43-year-old Military veteran in Clarksville, Tenn. “It does make it onerous to get out of debt. It looks as if you’re solely paying the curiosity.”

Ms. Dorsey has been working for years to chip away on the money owed she accrued when a sequence of well being points left her briefly out of labor. Now she is juggling three jobs to attempt to repay hundreds of {dollars} in bank card balances and different money owed. She is making progress, however excessive charges aren’t serving to.

“How am I purported to retire?” she requested. “I’m not in a position to save, have that rainy-day fund, as a result of I’m attempting to take down the debt that I’ve.”

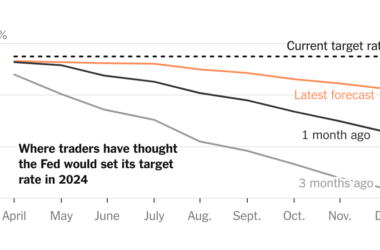

Ms. Dorsey isn’t more likely to get aid quickly. Fed officers have indicated that they count on to maintain rates of interest at their present degree, the very best in many years, for months. And whereas policymakers nonetheless say they’re more likely to minimize charges ultimately, assuming inflation slows down as anticipated, they might contemplate elevating them additional if costs start rising sooner once more. The most recent proof will come on Wednesday when the Labor Division releases information exhibiting whether or not inflation cooled in April, or remained uncomfortably sizzling for a fourth straight month.

The general financial system has proved unexpectedly resilient to excessive rates of interest. Customers have continued spending on journey, restaurant meals and leisure due to rising wages and debt ranges that, regardless of their current improve, stay manageable as a share of revenue for most individuals.

However mixture figures obscure an underlying divide that’s more likely to widen the longer rates of interest stay excessive. Prosperous households, and even many within the center class, have largely been insulated from the consequences of the Fed’s insurance policies. Many took out long-term mortgages when charges had been at all-time low in 2020 or earlier — in the event that they don’t personal their properties outright — and most have little if any variable-rate debt. And they’re benefiting from increased returns on their financial savings.

For poorer households, it’s totally different. They’re likelier to carry a steadiness on bank cards, that means they’re extra more likely to really feel excessive charges. Based on Fed information, about 56 % of individuals incomes lower than $25,000 carried a bank card steadiness in 2022, in contrast with 38 % of these incomes greater than $100,000. Black Individuals, like Ms. Dorsey, and Latinos are additionally extra more likely to carry balances.

Recent economic research suggests that top borrowing prices could also be one motive for Individuals’ dim view of the state of the financial system. In surveys, lower-income households stay significantly dour about their monetary well-being.

Barbara L. Martinez, a monetary counselor in Chicago who works at Heartland Alliance, a nonprofit group, stated that for a lot of of her low-income shoppers, debt is inescapable, particularly since meals costs and rents have soared. They don’t have financial savings to cowl sudden bills like automobile repairs or sickness. And whereas excessive borrowing prices aren’t essentially inflicting their monetary difficulties, they make coping with debt a lot tougher.

“You’re attempting to get out of the ocean, however the waves preserve pushing you again,” she stated. “Irrespective of how a lot you swim, you get drained.”

Excessive rates of interest are all the time harder on debtors than on savers. However more often than not, additionally they push down the worth of shares, homes and different property. Which means charge will increase often have an effect on households throughout the revenue spectrum, albeit in numerous methods.

That isn’t how issues have performed out not too long ago. Inventory costs fell when the Fed started elevating charges, however have rebounded and are close to a report. Residence costs have continued rising in many of the nation.

The result’s a rising divide. Fed information means that wealth for the higher half dipped after the Fed’s preliminary charge improve in 2022, however is once more setting information. For the underside half, nonetheless, wealth remains below its degree earlier than the Fed started elevating charges, after subtracting bank card and mortgage debt and different liabilities.

“Larger-income households really feel very flush,” stated Brian Rose, senior economist at UBS. “They’ve seen such an enormous run-up within the worth of their home and the worth of their portfolios that they really feel like they’ll preserve spending.”

Airways, accommodations and different industries that cater largely to higher-income customers have typically reported robust earnings of late. However mass-market manufacturers like McDonald’s and KFC have reported slower gross sales, with many citing weak point amongst low-income customers as a part of the explanation.

The divergence places Fed officers in an uncomfortable place: Free spending by rich households means excessive rates of interest have accomplished little to curb shopper demand. However with few different inflation-fighting instruments, policymakers have little alternative however to maintain rates of interest excessive — even when these insurance policies damage households which might be already struggling.

Virginia Diaz thought she was on observe for a safe retirement when she moved to Florida from New York almost 20 years in the past. However she drew down her financial savings and constructed up bank card debt serving to members of the family, together with a niece with well being points. Now excessive costs and excessive rates of interest are placing her retirement in jeopardy.

“Each time I make a cost to my bank card, many of the cash goes to pay curiosity, and that simply snowballs,” she stated. “I’m on the finish of my rope.”

Ms. Diaz, 74, stated she has minimize her spending to the bone — “If I wish to purchase a candle, I’ve to consider it,” she stated — and the remainder of her household can also be struggling. Her nephew, 35, works full time within the insurance coverage trade, however lives in an condo in her storage as a result of he can’t afford to purchase a home, or perhaps a automobile. A good friend of her niece’s additionally lives along with her, chipping in to pay payments.

Ms. Diaz virtually begged Fed officers to chop rates of interest.

“I do know they imply properly, but it surely’s not working,” she stated. “Decrease it, for God’s sake, so individuals can reside. Give us half an opportunity to provide us a good degree of residing.”

Many liberal economists agree, arguing that inflation has fallen sufficient that the Fed ought to begin chopping charges earlier than it causes extra extreme financial injury.

“Excessive rates of interest actually compelled cracks in that restoration, and it’s of us who’re on the margins of our financial system who’re hit first and hit hardest,” stated Rakeen Mabud, chief economist on the Groundwork Collaborative, a progressive group. “They actually function a bellwether for what may occur to the remainder of our financial system.”

However Fed officers argue it’s important to deliver inflation below management, partially as a result of it, too, has a much bigger affect on the poor, who’ve little room of their budgets to accommodate increased costs.

“In the event you’re an individual who’s residing paycheck to paycheck, and immediately all of the belongings you purchase, the basics of life, go up in worth, you might be in bother immediately,” Jerome H. Powell, the Fed chair, stated at a information convention this month. “And so, with these individuals in thoughts particularly, what we’re doing is we’re utilizing our instruments to deliver down inflation.”

And whereas excessive rates of interest have affected many households, they haven’t thus far triggered the widespread job losses that many progressive critics predicted and which have traditionally been hardest on lower-wage employees. The unemployment charge stays low, together with for Black and Hispanic employees, who are sometimes extra liable to lose their jobs when the financial system weakens. And wage development over the previous a number of years has been strongest for lower-paid employees.

For most individuals, “the large concern is whether or not you’re holding onto your job,” stated C. Eugene Steuerle, a fellow on the City Institute who has studied how financial coverage impacts inequality.

However excessive charges as we speak may make it tougher for a lot of households to construct wealth within the longer run by making homeownership harder. They may additionally curb the development of flats and homes, which over time may additional push up rents.

The consequence: a technology of younger adults who concern they’ll neither afford to purchase nor lease.

Chris Nunn, 31, has amassed greater than $6,000 in bank card debt, most of it from shifting bills tied to lease will increase. His lease in Louisville, Ky., retains rising, and he sees little hope of paying off the debt with what he makes driving for DoorDash whereas finishing a school diploma.

“We don’t have the credit score to have the ability to purchase a home, and we’ve got a bunch of debt, both scholar loans or bank card debt,” he stated. “So we’re trapped.”